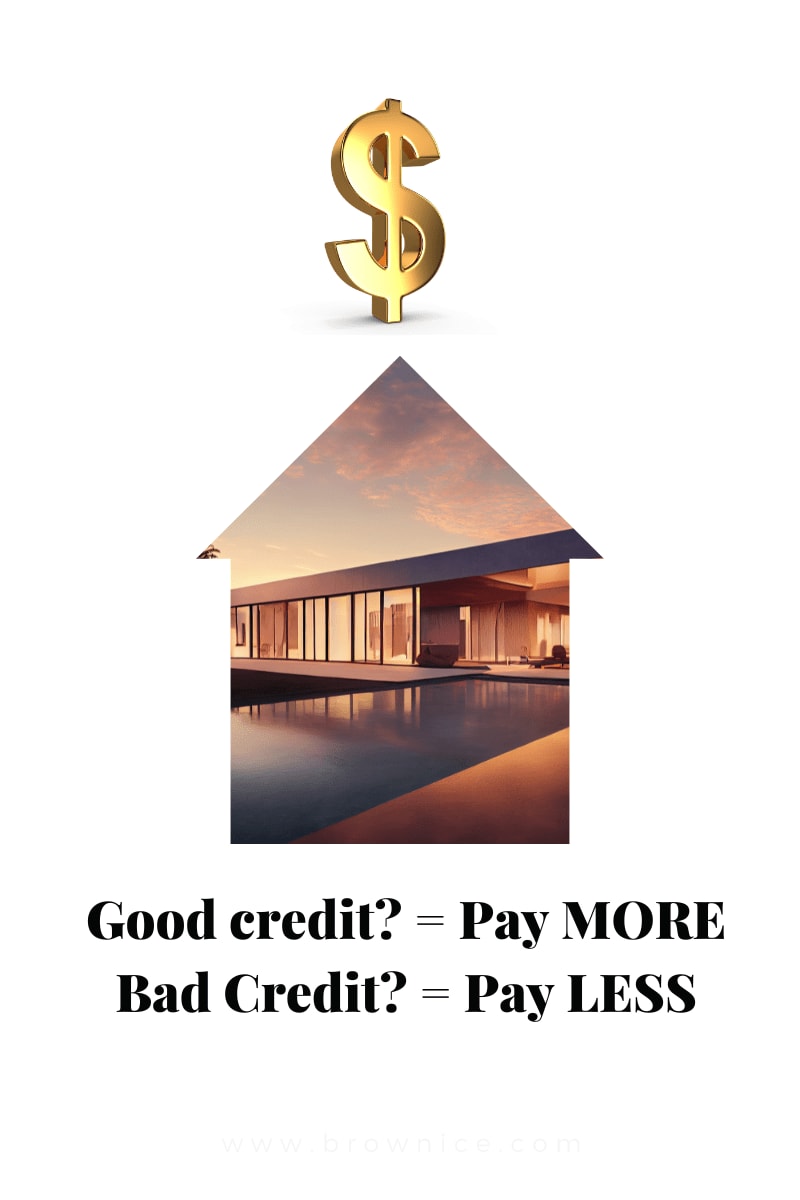

New rules for mortgage fees have been introduced by the Biden administration, which aims to provide equitable access to homeownership. However, these new rules may impact first-time homebuyers with high credit scores, who will have to pay more. The changes in the Loan Level Price Adjustments (LLPAs) mean that fees are based on several factors, including credit scores, size of down payment, type of home, and more. The FHFA introduced these new rules to promote sustainable access to homeownership, and it will affect loans backed by Fannie Mae and Freddie Mac, signed on or after May 1, 2023.

What does this all mean?

People with higher credit scores will pay more fees than those with lower credit scores under the new rules. However, the difference between the fees paid by people with good credit scores and those with lower credit scores will be smaller than before. This change aims to help borrowers who have been historically disadvantaged and have had difficulty accessing credit.

Homebuyers who put down a larger payment of 15% to 20% could see a bigger increase in mortgage fees. Still, this should not affect a borrower's decision-making process. Borrowers who put less than 20% down have to pay mortgage insurance, which offsets the lower upfront fee, so there is no financial advantage to putting down less than 20%.

How much will it cost me or help me?

The new fees are slightly more expensive for some borrowers with good credit and slightly less expensive for those with less-than-perfect credit. The penalty for having a lower credit score is now smaller than before, meaning that having a higher credit score or making a larger down payment is not as advantageous as it was before. The FHFA said that the new rules will redistribute funds to reduce the interest rate paid by less qualified buyers.

Critics argue that the new rules penalize people with good credit by using them to subsidize loans for riskier borrowers. They also fear that the new rules will encourage banks to lend to borrowers who should not qualify for a mortgage. While the changes may not address the ongoing inventory challenges in the housing market, mortgage fees still favor borrowers with good credit.

In conclusion, these new rules aim to promote sustainable access to homeownership by providing equitable access to mortgages. While people with higher credit scores may have to pay more fees than those with lower credit scores, the new rules will benefit less qualified borrowers by redistributing funds to reduce their interest rate. Despite the changes, mortgage fees still favor borrowers with good credit.